Taxes in the UAE for business: 9% corporate tax, 5% VAT and when you can pay 0%

The truth is that the United Arab Emirates tax system has made a giant leap in recent years from a full fiscal vacuum to a modern one

“There are no taxes in the UAE.” This phrase has become a mantra for many entrepreneurs around the world. And like any mantra, it is far from reality. The truth is that the tax system of the United Arab Emirates has made a giant leap in recent years from a complete fiscal vacuum to a modern, structured and, importantly, transparent system that meets OECD international standards.

Today, in 2026, doing business in the UAE and not thinking about taxes means dooming yourself to fines, account blocking and problems with the regulator. But the good news is that this system is still one of the most competitive and easy to understand in the world, if you know its rules.

In this article, the team Lien Advisors, with 5+ years of practical experience and a staff of specialized tax experts, will guide you through the three pillars of the UAE tax system: 9% corporate tax, 5% VAT and, most importantly, we will analyze who can pay 0% and under what conditions. You will learn not only theory but also how these rules are applied in practice to your business.

Part 1. Corporate Tax (CT) - 9% Income Tax

As of June 1, 2023 (for companies with a fiscal year beginning after that date), the UAE has a federal corporate tax. This is not a “tax on everything” but an income tax.

How does this work?

Rate: 0% for taxable profits up to 375,000 AED (approximately 102,000 USD). Anything above this amount is taxed at 9%.

Who pays: All companies (Mainland and Freezone) registered in the UAE, as well as foreign legal entities doing “regular business” in the country. The exception is the extraction of natural resources (it has its own rules).

What is calculated from: from net accounting profit reflected in financial statements prepared under IFRS standards (IFRS), with possible adjustments.

Critical nuances for entrepreneurs:

The AED 375,000 threshold is considered to be the cumulative total for the tax period (usually a year). This is not a monthly amount.

Losses can be carried forward to future periods and offset against future profits (with certain restrictions), which reduces tax.

Thin capitalization and TCO (transfer pricing). If you have loans from shareholders or deals with related parties (for example, your other company), the tax office will be careful to see whether profits are artificially underestimated. It is necessary to prepare transfer pricing documentation for major transactions.

Residency. A company is considered a tax resident of the UAE if it is registered here or is actually managed from the country (place of effective management). This is an important moment for international organizations.

Part 2. Value Added Tax (VAT) - VAT 5%

VAT was introduced in the UAE on January 1, 2018 and was the first major indirect tax. The rate is 5%, one of the lowest in the world.

The main rules of the VAT game:

Compulsory registration: If your company's turnover (revenue) over the past 12 months has exceeded (or is expected to exceed) AED 375,000, you must register as a VAT payer.

Voluntary registration: If your turnover exceeds AED 187,500, you can register voluntarily (this is often beneficial to be eligible for an input VAT deduction).

Mechanism: You charge VAT on your sales (Output VAT) and have the right to deduct the VAT you paid to your suppliers (Input VAT). Pay the difference to the budget (or get a refund if the input VAT is higher).

Zero rate (0%): applies to the export of goods and services outside the UAE, international transportation, the supply of certain investment metals, etc. This is not an exemption from reporting; you must report and prove your right to a 0% rate.

VAT exemption (Exempt): Certain activities (e.g. financial services, residential property rentals) are exempt from VAT. This means that you don't issue a VAT invoice, but you can't deduct VAT on your expenses either.

The main pain of business: VAT administration requires discipline. Invoices, records, declarations (usually quarterly). Penalties for delays or errors are significant.

Part 3. Holy of Holies: When can I pay 0% corporate tax?

This is where the fun begins. Many people think that “free zone = 0% tax always”. This is a dangerous misconception. The 0% rate for free zone companies is a benefit that must be earned and confirmed.

Qualifying Free Zone Person who is it?

To apply a 0% rate to its “Qualifying Income”, a free zone company must meet strict criteria and be considered a Qualifying Free Zone Person.

Main conditions (simplified):

Availability of the substance in the UAE: the company must have an adequate office, employees, and expenses. You can't be a mailbox.

Qualifying Income is income from:

Operations with other companies from free zones (B2B within the free zone).

Transactions with foreign counterparties (outside the UAE).

Certain types of activities approved for preferential treatment (production, cargo handling, logistics, etc.).

No “prohibited” income (Excluded Activities), 0% cannot be applied to income from:

Interactions with companies on the mainland (Mainland), except in some cases “de minimis”.

Banking, insurance and some other types of financial activities (unless you have a special license).

Real estate activities (except for some types of rentals in special areas).

De minimis rule: a company may lose the right to a benefit if its income from “inappropriate” activities (for example, sales to the mainland) exceeds 5% of its total turnover or a certain absolute amount.

Choice of 0%: The company must notify the tax authorities that it is a Qualifying Free Zone Person and wants to apply the preferential rate. This does not happen automatically.

What does this mean in practice?

If your company trades in a free zone only with foreign partners and sitting in your office - you are most likely to fall under 0%. If you sell your services to a local company on the mainland (for example, you are making a website for a Dubai restaurant), this income is likely to be taxed at 9%, and you need to be very careful whether you have exceeded the “de minimis” limits, otherwise you may fall under 9% all profit.

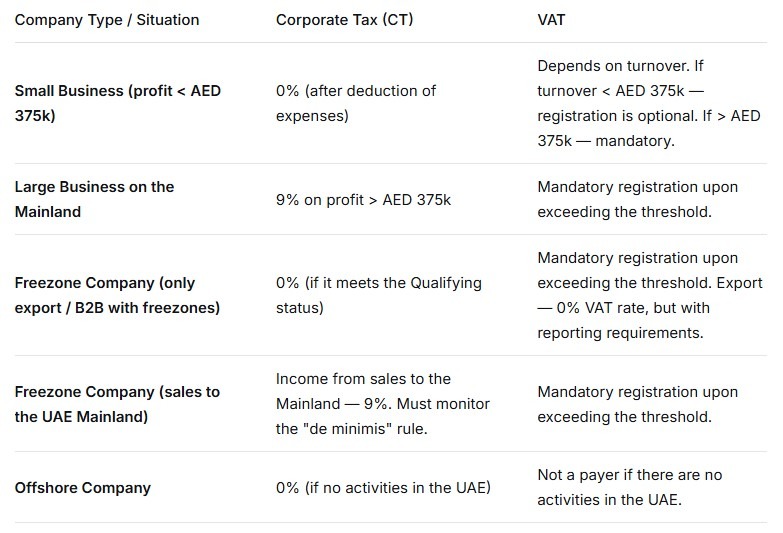

Part 4. Taxes and different types of companies: cheat sheet

Part 5. What do we need to do right now? roadmap

So that taxes don't come as a surprise, get into the habit of the following steps:

Forget the phrase “no taxes”. Take it as a fact that taxes are there. Their rates are low and the system is transparent, but they need to report.

Keep records from day one. Even if you have zero turnover. Use a simple accounting program or Excel, but record every transaction. Without accounting, you will not be able to calculate the tax correctly and confirm expenses.

Determine your tax status. Are you a Qualifying Free Zone Person? Are your activities subject to mandatory VAT registration? If you are not sure, please consult.

Meet deadlines. Penalties for late VAT or corporate tax returns are charged automatically. Mark all key dates on the calendar or delegate this to an accountant.

Document everything for the TCO. If you have deals with related parties (for example, you sell your own company's goods in another country), prepare transfer pricing files. The UAE Tax Service (FTA) is actively developing this area.

Part 6. Common mistakes in tax planning

We're in Lien Advisors we often see entrepreneurs falling into traps:

Mistake 1: assume that once the company is in the free zone, the 0% tax is guaranteed forever. No, your Qualifying status must be verified annually.

Mistake 2: Not registering for VAT even though the turnover has already exceeded the threshold. The penalties for this can be significantly greater than the tax savings themselves.

Mistake 3: Mixing personal expenses with corporate expenses. The tax office calculates income tax, and the director's personal expenses (going to a restaurant, shopping in person) do not reduce the tax base unless they are reasonable expenses for the company.

Mistake 4: Thinking that the Internal Revenue Service (FTA) is “sleeping.” The FTA is actively digitalizing and sharing data with banks and other regulators. The risk of verification, especially in case of high turnover or suspicious transactions, is high.

Conclusion: Taxes as part of a strategy, not a headache

Yes, the era of “tax paradise” in its classical sense for the UAE is over. But the era of tax transparency and predictability has begun. The 9% rate and the threshold of AED 375,000 still make the jurisdiction one of the most attractive in the world for legal, “white” businesses.

Success today does not lie in trying to “avoid” taxes, but in properly integrating them into your business model. Understand how much income you have is taxed at 0%, what is taxed at 9%, how to work with VAT and not run into fines.

In a team Lien Advisors we don't just help start a company. We are building a transparent operating model where tax strategy is an integral part. Our tax and compliance experts can help you:

Choose the right jurisdiction for your tax optimization.

Prepare for VAT and corporate tax registration.

Set up accounting so that reports are submitted on time and without errors.

Avoid risks associated with TCO and “prohibited” activities.

Do you want to understand how much tax you will actually pay and how to optimize the structure? Get in touch with us. We'll start by diagnosing your project, rather than trying to fit it into an outdated tax haven template.